Doing Business in Iran: A General Analysis of the Iranian Business Market with a specific section concerning the Italian Investments in the Country.

di Giovanni Coppola PhD Student in Management and Economics – Università degli Studi di Padova e Alessandro Spada

C.E.O. VRV Group e Vice-Presidente Assolombarda Milano e Monza-Brianza, Milano

ABSTRACT

As time elapsed and globalization advanced, many countries worldwide have started a development that seems limitless. The latter, called “Emerging Economies” have already overwhelmed in terms of GDP many of the most industrialized nations, and are preparing to become the economic stage of the future. Within this framework, investing has become harder; as it is true that market opportunities are crawling, it is also real that risks are numerous and cannot be undervalued. The work here presented and divided in 5 sections has the main aim of illustrating the latter, hopefully serving as a guide for future Italian investors in Iran.

(JEL Classification M16-F10-O11-E00)

Keywords: Iran, Business, Investments, Italy, Real GDP, Rouhani, Development

INDEX

1. Introduction 4

2. A Geopolitical and Historical Overview about the Country 7

2.1 Geopolitical Section 7

2.1.1 Some General Data about Iran 7

2.1.2 The Climate 7

2.1.3 The Population 8

2.1.4 The Administrative Structure 8

3. The Iranian Macroeconomic Framework 10

3.1 Iran’s Economic Structure 12

3.2 A General Analysis of the Iranian major Macroeconomic Indicators 14

3.2.1 The Gross Domestic Product (GDP) 14

3.2.3 Iran GDP Growth 16

3.2.4 The Country’s Debt Structure, Exchange Rate and Inflation 17

3.2.5 Rouhani Administration 22

4. The Investments’ Context and the Italian Role 23

4.1 Typologies of Investments 25

4.2 Foreign Direct Investments 28

4.3 Trade Relationship Italy-Iran 29

4.3.1 Percentage of Imports and Exports on Total 31

4.4 Firms and Future 34

5. Economic Previsions and Conclusions 37

BIBLIOGRAPHY 39

1. Introduction

In a historical period in which the Islamic Republic of Iran is at the center of international political debates, having a look to possible favorable scenarios towards our country can be useful. Italy in fact, has always occupied a prestigious position in the economic relationship with Iran, attesting as its first European commercial partner in terms of exportations and importations during the last years (The Observatory of Economic Complexity, 2017). However, it must be said that the relationships between the two countries have experienced up and downs during their history.

Due to the historic vicissitudes of their local populations, Italy and Iran have repeatedly met and crossed since ancient times. Starting from Sassanids and Parths in fact, political contacts with the Roman Empire were very frequent, although not always pacific. With the advent of Arabs in Persia, the geopolitical situation changed and relationships became almost null until the rise of Safavids brought back things on the right track.

Other than just political, relationship started to become even commercial during the Medieval Period, remaining such for many years. Persia in fact, due to its geographic position, played the role of intermediary in the commercial linkage that developed between Italy and China (“The Silk Route”), at the same time serving as a red carpet for the Marco Polo’s venture towards China in 1271. The latter, in his travel journal described (EINAUDI – Marco Polo (c.a.1298)): “Persia si è una provincia grande e nobile certamente. […] Quivi si fa drappi d’oro e di seta; e quivi àe molta bambagia, e quivi àe abbondanza d’orzo, di miglio e di pan(i)co e di tutte biade, di vino e di frutti.” (par. 30-32 Il Milione).

In the successive centuries, the Venice Republic entertained diplomatic rapports with the Iranian Khanats (territories under the control of a Khan – leader), sending several embassadors in the country.

Until the half of XIX century, the relationships remained unofficial also due to the lack of a more defined political framework in both countries. However, after 1862 year of the Italian unification, concrete commercial bilateral agreements started to be signed, with Iran that became a friend country (Trattato di Amicizia 1873). Afterwards, in 1886, the two nations opened the doors to their reciprocal permanent delegations.

Inevitably, the burst of the two World Wars brought to an interruption of rapports even because only Italy took active part in the conflicts while Iran declared its neutrality twice. At the end of the latter, things stabilized on a good level with the Italian President Giovanni Leone visiting Iran in 1977.

What happen successively has shockingly and negatively affected Iran’s position to the eyes of the world, reflecting to more actual events. With the beginning of the Iranian Revolution in fact, the filo-American Shah Mohamed Reza Pahlavi was forced to leave the country. That event led to a strong reaction of United States and a consequent diplomatic crisis between the two nations, even exacerbated by the appropriation of the American embassy in Teheran in 1979. The deterioration of this relationship brought United States to successively restrict the trade with what meanwhile had become the first Islamic Republic, implementing the famous “nuclear sanctions”. Iran in fact, during 50s and under the Reza Pahlavi regime had started the implementation of a nuclear program with the planning of a nuclear plant in Bushehr, initially with the sustain of some occidental powers (United States, France and Germany principally). The schedule however was delayed due to the revolution (1978-79) and the bombardment of Bushehr but retaken in 2002, this time with a different aim (the uranium enrichment) and the strong opposition of U.S. because of the aforementioned events.

Even if indirectly, what occurred conditioned the Italian confidence towards Iran. Italy, although characterized by small political groups supporting the Iranian Revolution, decided to ally with the more powerful United States, supporting the sanctions imposed as the European Union did too later. Another circumstance that contributed to a cooling of the previous harmony was represented by the Iran invasion of Iraqi troops leading to a conflict that lasted 8 years. Within this framework Italy although having some commercial partnerships with Iraq, declared its extraneousness, condemning the use of chemical weapons by Saddam’s soldiers.

Despite of that, last years have seen a reconciliation, with Italy that has offered its help in several reconstruction projects. Moreover, with the ultimate “Nuclear Deal” of 2015 and the consequent removal of economic sanctions, several new business partnerships have been set up.

The latter are the objective of the writing of this paper, which serves of the last available country data and is mainly structured in 4 different sections: a first one dealing with a geopolitical overview about the country; a second one describing the macroeconomic situation of Iran; a third one highlighting the Italian role for what concerns the investments in loco and a fourth one portraying some forecasts about the economic situation of Iran.

The hope is to provide a clear framework and a help to future investors, and especially Italian ones, in the Islamic Republic of Iran.

2. A Geopolitical and Historical Overview about the Country

2.1 Geopolitical Section

2.1.1 Some General Data about Iran

The Islamic Republic of Iran, situated in the middle-east area of the globe, expands on a surface of 164,819,600 km2 (18th largest country in the world). The country shares its borders with 7 states: Iraq in the west, Turkey in the northwest, Azerbaijan and Armenia in the north, Turkmenistan in the northeast, Afghanistan and Pakistan in the east; moreover it overlooks the Arabic Sea sharing the maritime confines with United Arab Emirates, Oman, Qatar, Bahrain, Kuwait, India, Saudi Arabia and the Caspian Sea with Kazakhstan, Russia. Therefore, Iran relishes a very strategic position that allows an enormous amount of trade even due to its richness in natural reserves of hydrocarbons, gas and crude oil.

2.1.2 The Climate

Iran, in general, experiences a climate of continental type with hot summers and cold winters, although the latter varies depending on the area (north is cooler while south it is hotter). The amount of rainfalls attests at more or less 250 ml per year on average and are mainly concentrated between October and April. In this sense, some exceptions are constituted by the Zagros plateau where precipitations raise to 500 ml per year on average and by the occidental part of the Caspian Sea where they can reach 1000 ml per year on average.

2.1.3 The Population

With a population of about 80 million (Population Pyramid, 2016), Iran ranks 17th when talking about the most populous countries. What leaps out is that the 60% of this sum is constituted by people that are younger than 30 years old and the 77% of the whole is literate. Taking into consideration this data and a forecasted 1.29% population growth rate, the country is expected to reach the 100 million units by 2050, intensifying the need for an occupation.

Currently 71.5% of the population lives in urban areas, contrary to the past (1950s) when more or less the same percentage lived in the countryside. This migration pattern has followed the same direction of many industrialized countries, reflecting the development and the need of modern products and services.

Between the people living in Iran, half are of Persian origin while a quarter is Azerbaijani. In addition to that also minority groups exist and are constituted by Bakhtyaris, Lors, Arabs, Armenians, Baluchis, Curds, Afghani and Turkmens.

The 99% of the overall professes the Islamism (10% Sunni, 89% Shia); the remaining 1% is formed by Catholics, Jews and Zoroastrians. The latter although protected by the National Constitution are however discriminated when looking for a public job.

The official language of the country is the Farsi, Azerbaijani is quite diffused too while Arab is spoken only in some areas of the South-West.

2.1.4 The Administrative Structure

Iran’s administrative structure is organized in 31 provinces called Ostan (Graph 1). Each of these provinces is divided into counties (Shahrestan, in total 299) which in turn are subdivided into 794 districts called Bakhsh.

IRAN ADMINISTRATIVE STRUCTURE

Graph 1 Iran

(Source: Major Tourist Attractions Map)

The Iranian political system is structured in two main pillars: the popular and the religious one. The first one provides for the simultaneous existence of a President of the Republic and a Parliament called Majlis, dependent on the Supreme Religious Guide and the Guardians Counsel which form the second regulatory organ. The Supreme Guide has the power on the armed forces and plays the role of ultimate decision maker in national affairs.

The Constitution of the Islamic Republic, in effect since 1979, considers the separation of power in executive, legislative and juridical as many of the Occidental countries’ do. In this sense, the executive power is given in custody of the President of the Republic, eligible for a maximum of two consecutive mandates of 4 years each based on an universal suffrage. The latter is the head of government and nominates 18 ministries which however can be distrusted and dismissed by the Majlis.

The Maljis is the legislative authority, constituted by 290 members (of which 5 representatives of minority ethnic groups) elected for 4 years. Their task is the proposal and approval of laws that however before becoming official must be accepted even by the 12 Counsel’s Guardians (formed by 6 theologians nominated by the Supreme Guide and 6 magistrates appointed by the Council of the Judiciary and approved by the Majlis), acting as the Italian Senate in this case.

The judicial power, exercised by the magistrates, is grounded on the Sharia (the Islamic Holy Law) and the positive law (comprising a civil and a penal code).

3. The Iranian Macroeconomic Framework

Since 1979, year of the Iranian revolution and of the establishment of the Islamic Republic of Iran, more than 30 years have elapsed and many things for the country have changed. Prior to Revolution, Iran could have been described as a ‘developmental state’. The Shah regime in fact, enjoyed autonomy from any social group and pushed towards policies aiming at the development of the private sector. The latter, had the main objective of strong creating growth, seen as the only phenomenon able to drag out the country from of a decades of underdevelopment and high poverty. To pursue this idea, Reza Pahlavi adopted a series of social and economic reforms simultaneously with an aggressive import-substitution industrialization policy to increase capital accumulation during 1960s and 1970s. Given its richness in natural resources, Iran had the great chance of emerging as an economy and the occurrence of the oil boom in the same decade (PIROUZ KAMROUZ, REZVANI FARAHMAND (2012)), fostered this vision. However, two main impediments in the end delayed this course of progression. First, the Shah’s strong submission and strict dependence on Western powers never gifted domestic political legitimacy to the regime; second, the irregular and non-uniform impact of economic growth in urban and rural zones in these years, raised social turmoils especially in the countryside. When this discontent ejected into the open air, the situation collapsed, helping all opposition movements concentrating against the Shah.

In this context, the role played by the mosques and religious groups activities, as unique entities spread all over the nation, became crucial. The Shiite faction was able to set a broad, cross-class coalition, which comprised the modern middle classes, the bazaar, the urban poor, the industrial workforce and other social groups. This extensive alliance ended the country’s relative independence from social groups and has been at the basis of the post-revolutionary state’s popular constituency. The two major ideals of the Iranian Revolution were achieving ‘economic independence’ and promoting ‘social justice’. Both were in direct contrast with the previous era’s focus on growth and development and set the road for the economic policy in the years to come. The strong anti-shah, anti-western fight and bombast of the Revolution reflected a rejection of the ancient regime’s strict reliance on external powers in general, and the USA in particular. The strong desire to make Iran an ‘independent’ economy, indeed, has been behind Iran’s pursuit of a generally autarkical development path since 1979, setting aside the globalization trends that have shaped the developing countries’ economies in recent decades.

In between this transition from a totalitarian regime to a democracy, the Iranian economy has been hit by a series of shocks, both internal and external. The latter were mainly consequences of major political events such as the revolution itself, the Iran-Iraq war, the still active economic and financial embargoes by the United States and by the European Union, the volatility of international crude oil prices and the uncertainties related to the exchange rate, once fixed and now floating. All of them, mixed to other factors have affected the long-term growth of the country, impeding the Iranian economy the exploitation of its full potential. Former Persia in fact, largely failed to capitalize on its special geopolitical location and its ample resources.

Nevertheless, the policy of the new elected leader Rouhani and the last events on the international stage such as the signature of the JPCOA, should ensure a bright economic future for the Iranians (Trump permitting) as all the major macroeconomic indexes described in this section, forecast.

3.1 Iran’s Economic Structure

As many other countries in the Middle-Eastern area of the world Iran is naturally endowed of gas (2nd country in the world for gas reserves), oil (3rd country in the world for oil reserves) and rare iron and non-iron ores (4th out of 10 countries). Under the most important classification systems, such as the World Bank one, at the moment it is considered as an economy in transition with a very young population and a low-medium average yearly per capita income amounting to 5000/6000€ (ICE).

Iran’s major economic activities are related to the exportation of hydrocarbons who represent the major source of public earnings (55% of the total budget in 2010 – ICE).

The industrial network is characterized by a strong presence of the National Government with many CEO’s that hold an office even at the ministry. As it is possible to imagine, the sector that is crucial for the economics of the country and is together the mostly regulated one, is the heavy sector, which comprises: oil facilities; chemical and petrochemical installations; iron and steel plants; road, naval and rail transportations; production and distribution of energetic sources; agricultural vehicles’ assembly; mines; aerospace and military industry.

The remaining part of the industrial network is formed by small and medium enterprises, mainly operating in the food and beverages industry (including the production of traditional products), footwear, clothing and textile sectors, electronics and machinery factories with a maximum number of 49 employees.

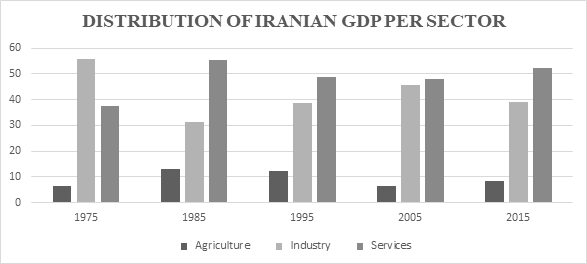

Ultimately, also banking sector services, although highly compromised by the international sanctions, have increased their incidence on the national GDP together with the telecommunications and projecting sectors (37.6% in 1975; 52.3% in 2015 – Graph 2). This result has been achieved mainly at the detriment of the industrial sector, which in 1975 accounted for the highest percentage of GDP expense (55.8%) while in 2015 attested at 39.1% as it possible to see from the below graph.

IRAN GDP EXPENSE DISTRIBUTION PER SECTOR

Graph 2 Iran

(Source: UNCTAD)

In the end, an important role for the country’s economy is even played by religious associations (BONYAD), instituted after the Islamic Revolution of 1979. The latter provide healthcare assistance in several hospitals, a help in popular houses, farming cooperatives and even in the touristic sector.

Counterposed to all of that, one of the major problems remains the involvement of government officials in the economic activities with obvious consequences in terms of efficiency of the market. The same authorities in fact are responsible for setting prices and quantities in various branches such as the energetic, agricultural and credit sectors.

3.2 A General Analysis of the Iranian major Macroeconomic Indicators

3.2.1 The Gross Domestic Product (GDP)

To understand the potential of a country, the first indicator that is always taken into account by economists – although not always so accurate – is the Gross Domestic Product, which calculates the total value of production of a country, taking into consideration only the final goods. The latter is usually presented in different forms such as GDP at current $ prices, at constant prices (adjusted for the effect of inflation) in local currency unit and corrected for Purchasing Power Parity.

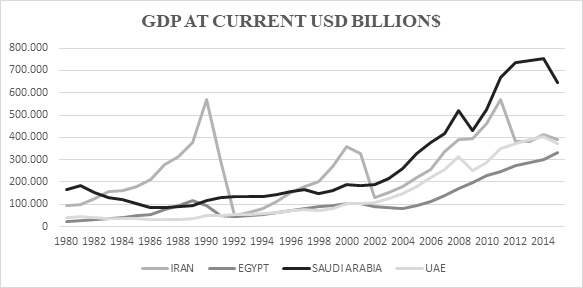

Talking in general, as it is possible to see from the graph (Graph 3 – IMF (2017)), Iran, after Saudi Arabia, can be considered the second biggest economy in within the Middle East and North Africa region (GDP current 412.304 billion $ IMF – 4.3% growth in 2016, expected 4.8% for 2017 – World Bank).

IRAN GDP AT CURRENT USD BILLION $

Graph 3 Iran

IRAN GDP AT CURRENT USD BILLION $

(Source: International Monetary Fund)

Considering the last 35 years, it is possible to frame Iran as having experienced three main peaks of economic boom: the first in 1990 due to an increase in oil earnings, that despite the period of global recession remained high, and the dismantling of strict controls on the market. In this period, many firms became private too. The second and the third peak were registered respectively in 2000 and 2011. The 2000 results were mainly the outcome of the introduction of Third Development Plan (ABBAS VALADKHANI (2001) – aiming at greater transparency in the macroeconomic system and regulatory frameworks, budget reforms, tax reforms, downsizing of the government’s role in economic activities and privatization of government enterprises, promotion of the private sector, dismantling of monopolies and promoting of competition and establishment of a comprehensive social safety net to protect the most vulnerable groups). The 2011 outcome instead, has been reached principally thanks to the Targeted Subsidies Reform, proposed by the president Ahmadinejad that increased the households’ disposable income, although creating a huge quantity of money in circulation causing problems in the successive periods (very low interest rates, too high and volatile prices leading citizens to spend soon and not to save).

Looking at the results of the other economies in the above graph, it is moreover possible to say that Iran has lost a lot of ground especially in the last decade, even considering that until 2001 and during some previous spans of time it has been the best performing economy between the four considered. It must be kept in mind that however all the data are not adjusted for inflation.

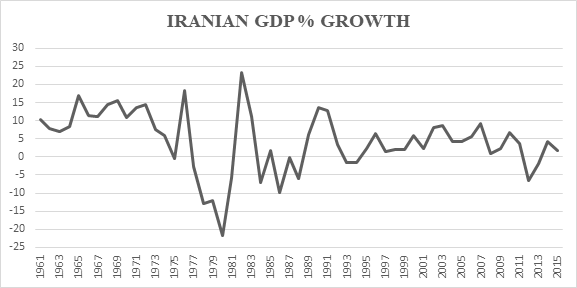

3.2.3 Iran GDP Growth

IRAN GDP % GROWTH

Graph 4 Iran

(Source: World Bank)

The Real GDP Growth rate is an indicator that measures economic growth in relation to the GDP of a country, adjusted for inflation.

As the graph portrays (Graph 4 – World Bank (2017)), the Iranian GDP real growth has since 1960 fluctuated within a range between -5% to 15% except for three time intervals: the first one compatible with the Iranian Revolution between 1978 and 1980 (-12.9% in 1979 and -21.6%, the lowest point, in 1980); the second one between 1980 and 1988, simultaneously with the burst of the Iran-Iraq war (in this case the only exception was represented by year 1982 in which the country experienced a 23.17% growth thanks to an upturn in the agricultural sector and an increase in oil prices – Middle East Research Institute); the third in 2012, considered as the worst financial year since the “imposed war”, due to the exacerbation of sanctions (SWIFT network exclusion) together with a huge increase in inflation (attesting at around 27.3%) and a high unemployment rate (12.2%).

After 2012 the GDP has started to grow again despite a flexion in 2015 caused by the last uncertainties around the signature of the nuclear treaty that nevertheless was in the last part of the year has been ratified. Economists have lately forecasted a rising percentage of growth of 4.2 and 5.6 for 2016 and 2017 respectively.

3.2.4 The Country’s Debt Structure, Exchange Rate and Inflation

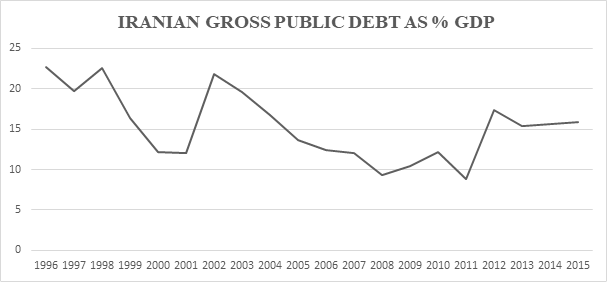

Starting from 1998 (Graph 5), due to an unanticipated drop in global oil prices and the consequent decrease in government revenues (the petrochemical industry had become nationalized meanwhile), the public deficit widened. Successively, we attend to a decrease in deficit until 2001 due to the new increase in oil prices and a more accurate expenditure policy. From 2002 until 2011 (except for a small upward in 2010), the Iranian government has been able to cut its public debt but as soon as the oil prices went down and the nuclear sanctions strengthened, the housing sector investments began to shrink and the trend inverted again. The construction and housing sector in fact, accounted for a good slice of the overall GDP production concerning industry expenses (around 20% in 2012) and enjoyed a great expansion starting from the first years of the new millennium. The national government in this case had to intervene by granting loans, which weighted on public treasury.

IRAN’S PUBLIC DEBT

Graph 5 Iran

(Source: International Monetary Fund)

From 2013, the public debt expense has more or less been constant but given the new political elections and the president Rouhani economic agenda focusing on cautious spendings, it is expected to decrease during the next years.

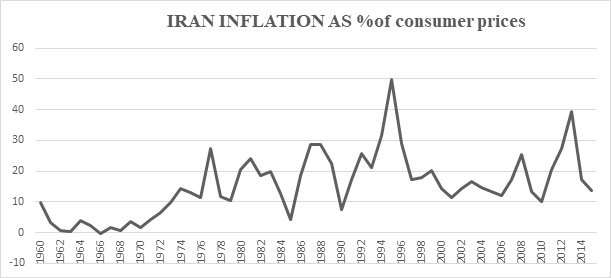

IRAN INFLATION

Graph 6 Iran

(Source: World Bank)

Since the birth of the Central Bank of Iran and so the first measurements, inflation for Iran has always been a huge problem to face for the national governments. The latter in fact is maybe the most volatile index that is characterizing the country and is still one of the major obstacles to the country growth.

By looking at the previous graph (Graph 6 – NEWS ABOUT IRAN (2012)) it is possible to see how during the whole 60s, given the Economic Stabilization Program, actuated by the government under the pressure of the International Monetary Fund and providing restrictions on imports and on government expenses, the level of prices did not fluctuated so much, making this period the lowest inflated of the Iran’s history. Problems instead started from 1974 on, and exacerbated during the successive decades due to wrong political decision (in 1974 the Shah decided to double the government expenditures) the successive Arab-Israeli war and oil embargo (1973-1974), the Iranian revolution (1979), Iraq`s invasion of Iran (1980-1988), Iraq`s invasion of Kuwait (1990), and the most recent political conflicts and Iranian energy, trade and financial sanctions. In general, Iran’s rapid inflation can be explained by the increase in production costs; the continuous growth of the demand for basic needs such as food and fuel; the inadequate supply of purified petroleum products and farm outputs; an heavy taxation on products imported that sometimes can even reach 100%.

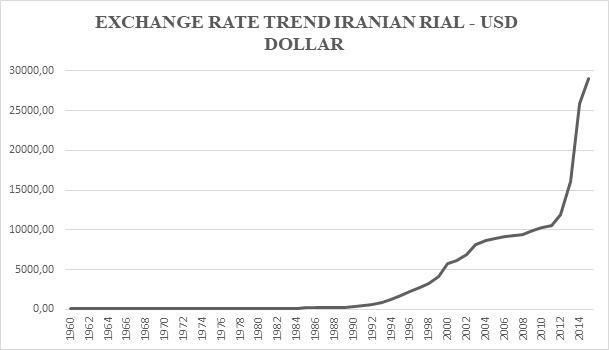

EXCHANGE RATE IRANIAN RIAL – USD DOLLAR

Graph 7 Iran

(Source: Federal Reserve)

Exchange rates (Graph 7) measure the price of a nation’s currency in terms of another. As soon as the financial markets started to function, Iranians decided to peg their currency to the British Pound (1932). After a series of appreciations and depreciation (the last one in 1942), it was decided to switch and peg to the U.S. dollar until 1975. During this time, the Iranian currency mostly appreciated, not depreciating even during the period of dollar devaluation in 1973.

The years successive to the Iranian Revolution marked a serious blow, with the Rial’s value declining precipitously after capital flights away from the country (71.46 rials for 1 dollar in the March of 1978; 9430 Rials for 1 dollar in the July of the 1999).

The successive new injection of foreign capital in the country caused the so called “Dutch Disease” with a loss of price competitiveness and so exports and an increase in imports. It looks like that starting from 2009 the Iranian Government intervened daily in order to let the exchange rate against the dollar to fluctuate within the range 9700-9900 (this mechanism is called managed float).

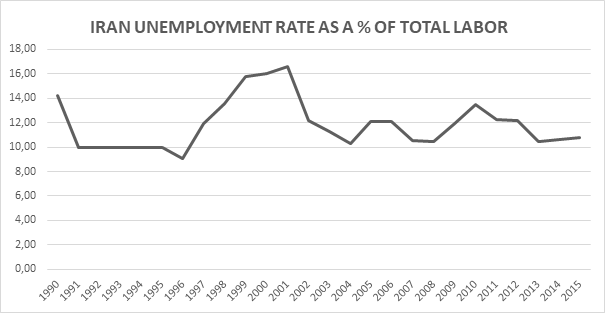

IRAN UNEMPLOYMENT RATE

Graph 8 Iran

(Source: International Monetary Fund)

Strictly related to the concept of inflation is the unemployment rate that starting from 1990 (Graph 8) has never lowered under 9% due to wrong government economic policies (Ahmadinejad) and increased business uncertainty.

Between 1991 and 1996 the unemployment percentage remained constant; afterwards the rate experienced an increase until 2001 when the first effects of the Third Economic Development Plan reverted the trend again.

Main causes for unemployment must be found in the following (ABBAS P. GRAMMY (2011)): the job market is highly dominated by public employments given the almost inexistence of totally private businesses, mostly of whom go bankrupted; the mismatch between Iran’s educational system and occupational needs (considering the teenagers 15-24 years old unemployment rate we reach an average of 26.2% of total labor force in 2016 – World Bank); college graduates classified as unskilled; state owned enterprises and government agencies are overstaffed and in debt; law that provides for employers to pay not less than a minimum wage, observe a limited number of hours of work, compensation for overtime, regular annual bonuses, social contributions, health and unemployment insurance costs, free training, housing and transportation expenses. For these reasons, employers in the last years are reluctant to hire permanent workers.

3.2.5 Rouhani Administration

More recently, the new Iran’s president Rouhani has inherited from the previous government an economic recession difficult to manage (-6.8% in 2012, -1.9% in 2013 – ICE) with a public debt greater than 100 billion $, an index of inflation greater than 30% and a devaluation of the Rial of more or less 200% (ICE).

Despite of that, the new head of State has quite soon been able to achieve significant improvements in terms of supply of basic necessities, reducing by a 20.3% the inflation (from 30% of December 2013 to 9.7% of April 2016 – ICE), stabilizing the exchange rate, and dragging away the country from the economic recession. The major contribution to this light economic recovery (3% for the Iranian Central Bank and 1.5% for IMF in 2014) has been generated by public investments for the general and infrastructural development of the nation, principally benefitting the most important firms operating under the control of the government (automotive, petrochemical, iron and steel).

However, the latter was not sufficient. In fact, due to the last 10 years very low oil prices and the consequent reduction in earnings; the reduction in the internal demand caused by a decrease of population purchasing power and the deferment of investment forced by the nuclear sanctions, the last Iranian Year (1394/2014 – individuated as the worst financial year for the country by experts) has registered a growth rate of 0%, confirming an economic stagnation that is going on even in the first months of 2017 (ICE).

This stagnation is mainly hitting the small and medium enterprises, facing a declining demand for goods such as cars, furniture, appliances but nevertheless has not negatively influenced the GDP in terms of PPP which instead has increased by 24 billion $ in 2014 (1.381 b. $ – ICE). Still Iran is considered the 18th largest economy of the world.

4. The Investments’ Context and the Italian Role

With the removal of sanctions and the consequent gradual exit from isolationism on the international markets, Iran represents a great opportunity for foreign firms who want to expand their business across the world. In fact, given the increase of in-ward and out-ward investments, the new commercial agreements (Graph 9 – SAEED K. D. – Iran’s Dealmaking with Europe (2016)) started with China (nuclear reactors), U.S. (Boeing) and European Union (Airbus, Danieli, Saipem, Total, Vinci, Peugeot, Aéroports de Paris and Bouygues), there should be no doubt about a prosperous future if the political situation will remain stable during the next years.

IRAN’S NEW COMMERCIAL AGREEMENTS

| CHINA | The Atomic Energy Organization of Iran (AEOI) and Chinese firms signed the agreement on redesigning the Arak reactor | |||||||

| UNITED STATES | Boeing: The pact worth 3 bn $ with Iran Aseman Airlines to purchase 30 of Boeing’s 737 Max planes adds to a separate $16.6 billion agreement with Iran Air, which the Chicago-based manufacturer is still finalizing. | |||||||

| EUROPEAN UNION | Airbus: Iran Air has ordered 118 commercial passenger planes including 12 Airbus A380s to renovate its fleet. The agreement amounted to 22bn € | Danieli: The Italian metal industry firm has signed a contract of 5.7 bn € to supply heavy machinery and equipment to Iran. | Saipem: The Italian oil and gas contractor has agreed a deal of 3.5 bn € to revamp and upgrade the Pars Shiraz and Tabriz oil refineries. | Peugeot (400m): The French carmaker made a deal for a joint venture with the Iranian vehicle manufacturer Khodro to modernize a car factory near Tehran, where three new Peugeot models will be manufactured. The two companies worked together before sanctions, and the project will produce 100,000 vehicles a year starting in late 2017. | Total: The oil giant signed a contract with the national Iranian oil company to buy as many as 200,000 barrels of crude oil per day (€6.6m at current prices), according to the French firm’s chief executive, Patrick Pouyanné. | Vinci: The Italian construction firm will develop a new terminal at Shahid Hashemi Nejad airport in Mashhad, north-east Iran. | Aéroports de Paris and Bouygues: The French company will assist in the construction of a second terminal at Tehran’s Imam Khomeini international airport | |

(Source: The Guardian)

4.1 Typologies of Investments

Article 3 of the Iran’s Foreign Investment Promotion and Protection Act (FIPPA), portrays the following possible investment methods for Iran: (i) Foreign Direct Investment (FDI) in areas with no bans on private sector activities; (ii) Joint-ventures, iii) buy-backs and iv) build-operate-transfer(BOT).

i) Foreign Direct Investments in Iran:

The Foreign Investment Promotion and Protection Act (FIPPA), establishes for the possibility of the following FDIs:

Establishment of a new Iranian company or purchase of shares of an existing one

Through contractual arrangements between the parties with or without formation of company.

The direct investments in the private sector will only be authorized in accordance with the Act.

Article 3 of the FIPPA moreover provides that foreign investment in sectors monopolized by the government will only be possible if no public money guarantees are ensured to these entities.

Under article 44 of The Constitution of the Islamic Republic of Iran: “The state sector is to include all large scale and mother industries, foreign trade, major minerals, banking insurance, power generation, dams, and large scale irrigation networks, radio and television, post, telegraph and

telephone services, aviation, shipping, roads, railroads and the like; all these will be publicly owned and administered by the State”.

ii) Joint Venture:

Provides for the establishment of a commercial partnership between two or more entities. This model, decreases risks and costs of investing, however it is subject to a series of requirements. The best choice between the two models depends on the hosting country legal system.

In various legal systems, the Joint Venture can attain different denominations such as partnership” “consortium” and sometimes “shareholders agreement”. For Iran, Article 3 of FIPPA allows for a corporative joint venture or a contractual joint venture. In the corporative joint venture, partners establish an independent legal entity, dividing the shares between the participants to the business. The latter are called shareholders and are the ultimate responsibles of the business project. On the other hand, the contractual joint venture it is an agreement just based on contracts, which does not create a new company.

iii) Another investment method presented in the FIPPA is the “buy-back” that in recent year has played an important role in the Iranian economy. The latter is mainly utilized in businesses concerning the development of oil and gas sites.

Buy-back can be defined as a contractual agreement between two parties, a vendor and a purchaser, in which the vendor commits to re-purchase back the good sold to the purchaser in case a certain event occurs in a specific period of time. The price is established at the moment of the signature of the contract. Buy-backs are regulated under article 2 of the Executive Iranian Rules and are usually utilized for the development of oil and gas fields in Iran.

iv) The last contractual framework for investment is the “Build, Operate, and Transfer (BOT) Contract”. This methodology of investment is usually chosen for building infrastructures such as roads, power plants, airports and telecommunications. BOT contracts concessions are conferred by governmental entities for specific projects in the private sector. The private party is responsible for the design, supply, finance and management of the overall project. During the project period, the private entity is entitled to sell the outputs. At the end of this time, the ownership of the plant is transferred to the government free of charge. In the end, the BOT contract it is a mixture between a private and public partnership in which the government decides to give custody of a specific project to a private party. It is a fast and cost-effective investment option provided that the private firm is accurately chosen.

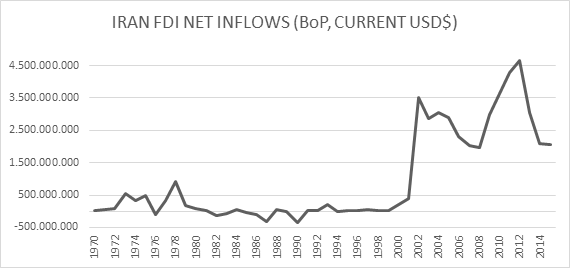

4.2 Foreign Direct Investments

IRAN’S FDI INFLOWS

Graph 10 Iran

(Source: World Bank)

The FDI it is a kind of investment where a foreign entity puts some money in a business across borders in order to achieve long-term profits.

As portrayed by the graph (Graph 10) the two periods in which Iran enjoyed the most part of foreign direct investments coincide with the Shah regime and the first years of the new Millennium. Taking into consideration the internationally oriented economic policy undertaken by the shah the results for the period 1973-1979 should not surprise so much; instead, it is worthwhile to understand why in 2002 the FDI boomed. The reason must be found in economic reforms actuated by the government, which comprised the exchange rate unification, trade and tax reforms, and ratification of the law on foreign direct investments.

4.3 Trade Relationship Italy-Iran

As stated at the beginning of this work, Italy and Iran nourish good relationship since ancient times. The latter, together with some cultural similarities (Iranian civilization is closer to the Italian one with respect to other Middle-Eastern countries) has contributed, during the last years, in making Italy the first European commercial partner (Financial Tribune (2017)). The peninsula has been able to achieve this position in a period of strong trade difficulties, reaching a volume of 400 million euros of exports towards the country in 2017. This numbers are destined to increase during the next years with a forecasted 2.5 billion euros of exportations towards Iran within 2019 (SACE).

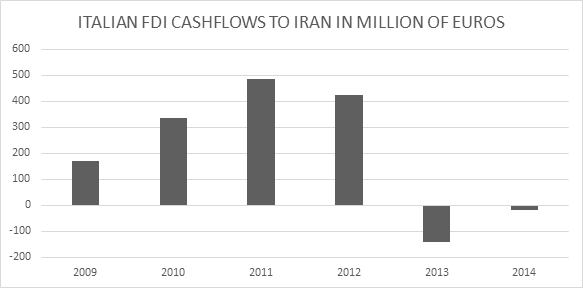

ITALIAN FDIs TO IRAN

Graph 11 Iran

(Source: ICE/ISTAT, 2015)

The last available data on Italian FDI (Graphs 11 – Table 1) directed to Iran portray a huge difference in terms of millions of euros invested until 2012 and after, when the sanctions have been strengthened. However, given the latest events, for the next years economists forecast a phase of upswing.

TABLE 1

| 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |

| Exports to Iran | 2.013 | 2.059 | 1.863 | 1.407 | 1.065 | 1.155 | 1.210 |

| Variation% | 2.3 | -9.5 | -24.5 | -24.3 | 9.3 | 4.8 | |

| Imports From Iran | 1.968 | 4.745 | 5.327 | 2.239 | 137 | 440 | 468 |

| Variation% | 141.1 | 12.3 | -58 | -93.9 | 220.6 | 6.3 | |

| TRADE BALANCE | 44.9 | -2.686 | -3.464 | -833 | 919 | 715 | 742 |

(Source: ICE/ISTAT)

4.3.1 Percentage of Imports and Exports on Total

By looking at the tables below (Tables 2-3 – The Observatory of Economic Complexity (2015)) it is possible to realize that even the flow of Italian imports from Iran and exports to Iran has been highly affected by the introduction of sanctions. Exports in fact show a decreasing trend starting from 2011 with just 2015 that marks a positive variation with respect to the previous year (+4.8%). Imports instead started a decline in 2012 and as imports only in 2015 registered a positive change (+6.3%). Last statistics however (2017) portray Italy as even the first European imports’ commercial partner of Iran with France ranking second and Germany third.

TABLE 2

| China | 41% |

| South Korea | 8.6% |

| Turkey | 8.2% |

| India | 7.1% |

| Germany | 5% |

| Brazil | 3.8% |

| Italy | 3% |

| Russia | 2.3% |

| Switzerland | 2.1% |

| Argentina | 1.6% |

| France | 1.4% |

| Kazakhstan | 1.3% |

| U.K. | 1.2% |

| Malaysia | 1.1% |

| Netherlands | 1.1% |

| Others | 11.2% |

(Source: Atlas Media, 2015)

TABLE 3

| China | 45% |

| India | 18% |

| Japan | 9.1% |

| South Korea | 6.6% |

| Turkey | 4.1% |

| Afghanistan | 3.2% |

| Italy | 1.5% |

| Hong Kong | 1.2% |

| Germany | 0.9% |

| Others | 10.4% |

(Source: Atlas Media, 2015)

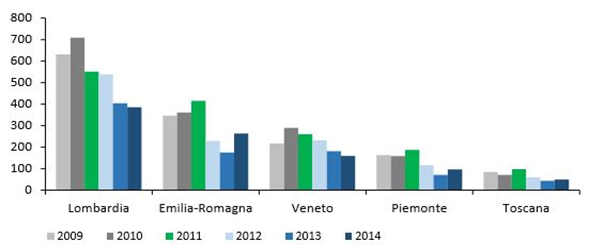

4.3.2 Regional Exports to Iran

ITALIAN REGIONAL EXPORTS TO IRAN

Graph 12 Iran

(Source: ICE/ISTAT (millions of euros), 2015)

2014 Regional Italian data concerning exports to Iran (Graph 12) depict Lombardia (approximately 400 million euros) as the major source of interchange between Italy and Iran, followed by Emilia-Romagna (approximately 300 million euros of exports), Veneto (approximately 180 million euros of exports), Piemonte (approximately 100 million euros of exports) and Toscana (approximately 50 million of exports). This ranking has remained constant during the years 2009-2010-2011 and 2014 while 2012 and 2013 Veneto region found itself at the second place in terms of exports to Iran at the detriment of Emilia Romagna. Despite of these data what is important to portray is the decreasing trend that characterizes the regional amount of exports’ expenditures starting from 2011 and until 2013. Ultimately, just 2014 has registered an increase in spending for Emilia Romagna, Piemonte and Toscana with respect to the year before. The latter reduction may be explained by the firms’ unwillingness to trade with Iran after the enforcement of sanctions given the possibility of being inserted in a black list.

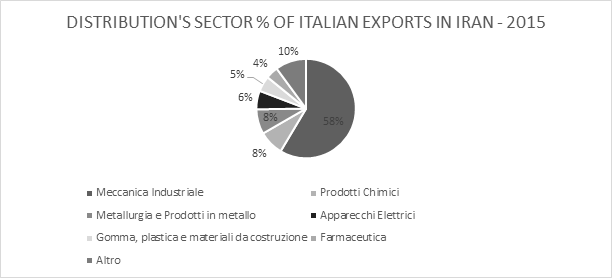

4.3.3 Products

PRODUCTS EXPORTED TO IRAN

Graph 13 Iran

Fig. 25 (Source: ICE/ISTAT)

The pie chart (Graph 13) shows the typologies of product that Italy exports to Iran as a percentage of the total exportations. As it was not so difficult to imagine, Iran imports to us mainly mechanical engineering technologies; other products account for 10% or less on the overall.

4.4 Firms and Future

Many Iranians and economists would have expected a rapid recovery after the removal of sanctions but in reality things did not performed as expected as is it also possible to see from latest protests. Due to the ongoing political tensions with United States (with which relationships deteriorated after the throwing out of the shah and the hostage crisis accident), a strong ally of the Saudi Arabia, Iran is in a situation of stall. Many of the businessmen to which I have been asking about how to conduct a business in Iran or with Iran have more or less reported the same problems. Dr. Spada, CEO of VRV – a firm specialized in the production of petrochemical and gas storage products – with whom I had a speech some months ago, illustrated me how the way of doing business with Iran has changed with respect to the period previous to the sanctions’ introduction. He said: “Iran has always been a good market for VRV given its peculiarity and strong reliance on oil and gas sector. Many of our clients (such as Saipem and Technimont) signed huge contracts with Iranian firms for the exportation of petrochemical product but as soon as sanctions started to be implemented, they began to back up or even stop temporarily to trade with Iran. Nowadays, after the removal of sanctions many of them are approaching again the market”.

“For us the situation has been a little bit different since we sell components and although we had to start to pay more attention on if the purchaser of our products was under sanctions, we were able to continue to work in Iran with the authorization of the Ministry of Economic Development. During these years, the turnover has decreased but at the same time even the competition became less fierce. What is sure is that difficulties have exponentially augmented. Sometimes has even been difficult to receive money after having sold the products.”

The CEO Spada in the end has launched a message of opportunity for the people who want to invest in Iran: “the oil and gas sector but also the infrastructural one will for sure represent a business chance during the next years although a strong financial and political risk persists. Nevertheless, Italian firms have all what it takes to pursue prestigious projects.”

During my business trip to Tehran, I also had a very interesting chat with two Iranian entrepreneurs in the oil industry Mr. Masood Shaikh (Persol Corp.) and Mr. Atoosa Biglari (Mohsen Int. Trading Co.). The latter portrayed me all the present difficulties in conducting an international business in Iran: “at present times we are having a lot of trouble for importing the raw materials and then export our outputs. Some of the European firms with which we had commercial accords, suddenly stopped the furniture of products to us because of the fear to be placed in black list if caught at doing business with our country. Furthermore, sometimes we have problems in repatriating our profits when exporting the products because payments towards Iran are blocked. The only solution would be to open up a bank account in Europe and directly re-invest this money, but no bank accepts us due to the sanctions. So at the moment we have decided to open an account in China”.

Problems however extend also to the relationship with public administration: “the information system does not work very well in Iran and just some days ago (May 2017) we had one of our orders from China blocked at the customs because on the box containing the products there was no label indication the contents. The law had changed few time before but we did not know about that because no one adviced us!”.

Last words had inflation as a topic: “Inflation and exchange rates in Iran are really really crazy, there have been periods were prices went up even daily and exchange rates changed every minute. This uncontrolled phenomenon is mining the whole economic system. One day for example we pay an order of 10000$, the day after for the same order we pay 12000$; this also obliges us to then increase the final price of our products.”

Further tips have been kindly released to me by Dr. Esmaeil Karimian, founder and managing partner of ESK Law Firm. He, together with Saleh Jaberi (Head of Contractual Team) and Saeid Soltani (Head of Corporate Team) is the author of a book titled “Doing Business in Iran” which explains all the financial and legal aspects to be considered when investing in Iran. Dr. Karimian remarked that: “the choice about the best way to invest depends on the project criteria and specification a person is dealing with, but the subsidiary is for sure one of the best methods since gives you a series of advantages such as owning land, opening a bank account and enjoying a better control of the local environment. Ultimately, the most part of foreign investments are concentrated in the oil & gas sector, which is the most profitable in Iran, but also renewable energy sector is catching a good slice of the market.”

Dr. Karimian, as Mr. Shaikh and Biglari has highlighted too the problems faced when trading: “Many of our banks are still excluded from the SWIFT system and it is very difficult for us to opening bank accounts or receiving money. The solution is to use Sarafi (private institutions) or use an intermediary bank of an Asian country from whom repatriate profits to Iran.”

Then, talking specifically about the Italian investments in Iran, he said: “ESK law firm has had some contacts with Italferr Company for the construction of a high speed railway system; however Italians did not accept our proposal due to budget limitations. In general is not so easy to deal with Italians for the latter reason.”

Dr. Karimian in the end concluded with his though about the evolution of the Italo-Iranian economic relationship: “After the repression of International sanctions, Italian companies has slowly started to invest again in Iran. However, the repulsion to make business here still remains since United States are still fully keeping an eye on us. Nevertheless I expect an increase in the amount of trade between Italy and Iran, also given Trump’s further closure of the American market to the Middle-East.”

From these witnesses it is easily understandable that although sanctions have been removed and the JCPOA has been signed, still a lot of time will be needed to make Iran a completely free and internationally integrated market.

5. Economic Previsions and Conclusions

How it is possible to imagine and how many economic previsions’ institutes and experts portray, the suspension of economic sanctions will definitely help the country’s economy. It is estimated that during the next two years (2017-18), Iran will experience an economic growth between 3-4% (IMF).

This overlook will come out from the many contracts and agreements closed after the “implementation day” that at that point will be effective, boosting investments and private spending.

The World Bank instead has forecasted for Iran an economic growth of 5.2% for 2017 . These previsions are based on the fact that:

• The national production of oil will reach the 4.2 million of barrels per day in 2017.

• Oil exportations should increase by 0.7 million barrels per day in 2017 (at least if no foreign companies will invest in the region such as the French Total is willing to do)

• During the next years, it is possible that the exportations of gas, petrochemical products and manufactured products will significantly increment.

The major challenges that the Rouhani government should keep facing after the relief of nuclear sanctions are related to the improvements of economic indicators and the creation of job places that in turn necessitate an expansion of the purchasing power of households obtainable through an increase of salaries; greater investments by the government and major availability of money supply by banking institutions.

Uncertainty remains very strong. In fact, as Europe has decided to continue its dialogue with Iran started 2 years ago; Israel and Saudi Arabia squared up again as enemies, together with the giant noose of the United States that under Trump have implemented new sanctions for the Iranian use of missiles (February 2017) and seem wanting to freeze the Nuclear Deal signed in 2015 under Obama administration. Times are still unfavorable, but for the future it is out of any doubt that the country has the power to come out from the darkness.

BIBLIOGRAPHY

ABBAS P. GRAMMY (2011) – The Misery of Unemployment and Inflation in Iran. Available from: https://www.csub.edu/kej/_files/MiseryofUnemployment.pdf

ABBAS VALADKHANI (2001) – An Analysis of Iran’s Third Five-Year Development Plan. Available from: http://ro.uow.edu.au/cgi/viewcontent.cgi?article=1422&context=commpapers

CHIARLONE S., HELG R. (2002) – Il modello di specializzazione italiano e le economie emergenti dell’estremo oriente. Available from: http://arl.liuc.it/dspace/handle/2468/2339

EINAUDI (Marco Polo) – Il Milione. Available from: file:///C:/Users/Giovanni/Downloads/Milione.pdf

FINANCIAL TRIBUNE (2017) – Italy biggest EU Trade Partner of Iran. Available from: https://financialtribune.com/articles/economy-domestic-economy/64802/italy-biggest-eu-trade-partner-of-iran

HADI SALEHI ESFAHANI, M. HASHEM PESARAN (2008, pag. 1-26) – Iranian Economy in the Twentieth Century. Available from: http://faculty.las.illinois.edu/esfahani/IndexFiles/Esfahani%20and%20Pesaran%20-%20Iranian%20Economy%20in%20Twentieth%20Century.pdf

INDEX MUNDI (2014) – Merchandise Imports. Available from: https://www.indexmundi.com/facts/iran/merchandise-imports

INDEX MUNDI (2014) – Merchandise Exports in Iran. Available from: http://www.indexmundi.com/facts/iran/merchandise-exports

INTERNATIONAL MONETARY FUND (2017) – World Economic Outlook. Available from: http://www.imf.org/external/datamapper/NGDPD@WEO/OEMDC/ADVEC/WEOWORLD/IRN

INTERNATIONAL TRADE CENTER (2016) – Iran Trade Map. Available from: http://www.intracen.org/layouts/CountryTemplate.aspx?pageid=47244645034&id=47244652059

KNOEMA (2016) – Inward and Outward Foreign Direct Investment Flows and Stock. Available from: https://knoema.com/UNCTADFDI2016/inward-and-outward-foreign-direct-investment-flows-and-stock?location=1001000-iran-islamic-republic-of

KNOEMA (2017) – World Development Indicators. Available from: https://knoema.com/WBWDIGDF2016Oct/world-development-indicators-wdi?tsId=3330730

NEWS ABOUT IRAN (2012) – Economic History of Iran: Pre-Islamic Revolution. Available from: https://iransnews.wordpress.com/2012/01/31/economic-history-of-iran-pre-islamic-revolution/

PIROUZ KAMROUZ, REZVANI FARAHMAND (2012, par. 3) – Evaluating the Iranian Economy 2000 to 2010. Available from: http://www.freepatentsonline.com/article/Review-Business-Research/293950206.html

SAEED K. D. – Iran’s Dealmaking with Europe, THE GUARDIAN (2016). Available from: https://www.theguardian.com/world/2016/jan/29/irans-dealmaking-europe-seven-biggest-contracts

STATISTA (2016) – Iran: Import of Goods from 2006 to 2016. Available from: https://www.statista.com/statistics/294360/iran-import-of-goods/

TEHRAN TIMES (2017) – World Bank forecasts 5.2% GDP Growth for Iran in 2017. Available from: http://www.tehrantimes.com/news/409962/World-Bank-forecasts-5-2-GDP-growth-for-Iran-in-2017

THE IRAN PROJECT (2016) – IMF expects 6.6% economic growth for Iran. Available from: http://theiranproject.com/blog/2016/12/20/imf-expects-6-6-economic-growth-iran/

THE OBSERVATORY OF ECONOMIC COMPLEXITY. (2015) – Iran Commercial Profile. Available from: http://atlas.media.mit.edu/it/profile/country/irn/

WORLD BANK (2017) – The Islamic Republic of Iran. Available from: http://data.worldbank.org/country/iran-islamic-rep?view=chart

{kind=link}