How the endowment effect and the framing effect affect consumer decisions process

Abstract

We already know from behavioral economics, which is opposed to classical economics, that when people take actions based on psychological phenomena, instinct and emotions, this is not optimum. So that, they are pushed to implement complex strategies to manage. In classical economics, investors and consumers are considered hyper-rational and calculating, in possession of all the information necessary to make their choices and oriented towards maximum utility and profit. Instead, in behavioral economics the subjects are often altruistic, with changing preferences over time. Under the influence of emotional factors, they are often lead to make risky choices that do not maximize their usefulness.

In this article we want to go a step further, introducing two other aspects closely related to behavioral finance, called “endowment effect” and “framing effect”.

Endowment effect

The endowment effect is the principle according to which we tend to attribute a higher value and therefore a higher price to the things we already own. This mental strategy is due to the fact that, when we decide to sell or evaluate an asset we own, we tend to attribute a higher value than the market does, increasing it by an “emotional value”. The Israeli psychologist and economist Daniel Kahneman, Nobel laureate in economics in 2002, conducted an experiment aimed at verifying whether the value we attribute to our assets always follows objective logic. The experiment consists in seeing the logic of selling and buying a mug, taking a group of people and dividing it into three subgroups, sellers, buyers and choosers, each with a specific function. I propose again Kahneman’s example, in order to give an explanation of the principle underlying the decisions made irrationally by consumers [1].

- Sellers are those who have to attribute a value to an asset, in this case a mug, to which they have no emotional relationship, and try to sell it;

-

Buyers must give a value to the mug, and indicate at what price they would be willing to buy it;

-

Choosers, who must also give a value to the mug and choose whether to buy it or receive the equivalent in cash.

According to the experiment, sellers attribute a value to the mug of about $ 7, while both buyers and choosers value the mug at around $ 3, which is less than half the price set by the sellers. The result is that the simple fact of owning something leads to attribute a higher value to it, about double what one is willing to buy it far on the market. Simply owning something makes your mind think it is worth more.

But what is the reason for this price difference? The fact is, people value an asset they own more than something they don’t own, and that’s what behavioral economists call “endowment effect”. Researchers have proposed different reasons for this effect, that may be explained by psychological components related to loss aversion [2].

The endowment effect is applicable to various areas. For example, a stockholder who needs cash is pushed to refuse to sell his stocks when they are worth less than when he bought them, or still the owner of a property purchased for $ 240,000 is against to sell it for a lower value than what he paid for it, although the real estate market has undergone a general decrease of 20%. For him the “fair value” of the asset would be given by the sum of the purchasing price plus a sentimental value. This shows quite clearly that reasoning strategies and emotions can therefore lead us to make non-optimal choices, whereas the aspect that should be taken as a reference is the current market price of the asset [3].

Taking the example of the property and turning it upside down, another buyer would not be willing to buy the same property at 20% extra.

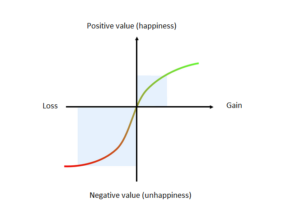

When you need to sell an asset (house), the market price is the determining factor, not the purchase price. Likewise, behavioral economists have shown that losing is about twice as much pain as the happiness we feel when we make an equivalent amount of money. For example, if we lose $ 5, we must earn at least $ 10 to be happy again.

Framing effect

The second effect I want to talk about is the so-called “framing effect”, the result of the study of the two psychologists Amos Tversky and Daniel Kahneman, according to which the way or the context in which a problem is presented to us influences our decisions.

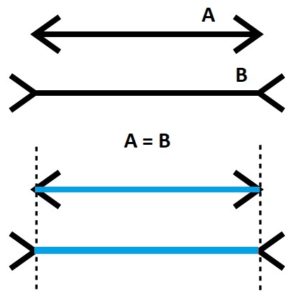

Cognitive distortions, in fact, are able to induce our mind to formulate solutions contrary to logic, putting in place mental shortcuts that we do not even realize. A very simple but useful example to understand the framing effect is the Müller-Lyer illusion.

Looking at the two lines, we first have the perception that the second is longer than the first one, while instead they have exactly the same length. The only difference between them is the way in which the segments are arranged.

This simple example demonstrates that just as the ends of the lines influence our choice between which one appears shorter or longer, in a several matters our estimates are often influenced by external factors that have no direct bearing on them. The framing shouldn’t affect us in any way, but it often does [4]. Behavioral economists refer to choices influenced by the situation in which we find ourselves or by the world in which a problem is described to us as “framing effect”. From an economic-financial perspective, the context in which a problem is described to us can be incisive on how me make our investment choices [5].

A well-known high case that refers to the framing effect is the bet vs lottery test [6]. An individual is asked to choose whether to accept a bet with a 10% chance of winning $ 95 and a 90% chance of losing 5, or participate in a lottery, whose ticket costs 5, with a 10% chance of winning $ 100 and a 90% chance of not winning. In most cases, people tend to prefer the lottery, when actually there is no better decision from an economic point of view, as in any case the loss would always be $ 5 (the price of the lottery ticket) and the payout is always 95 dollars. In any case, therefore, the only choice to make is whether to aim to become richer by $ 95 or poorer by $ 5. Also this example shows that a different presentation of the problem influences the choice people make.

Conclusions

Individuals are typically loss averse, meaning they are much more sensitive to the possibility of losing than the possibility of earning a certain amount. In other words, the emotional reaction to losses is systematically stronger than the reaction of earnings of the same amount. People also suffer from the so-called “myopic loss aversion” [7], the attitude of neglecting long-term perspectives to focus on short-term ones, cutting down their fear of suffering losses.

For this reason, carefully assessing the time frame and the risk tolerance are important factors in choosing the right assets to invest in.

(a cura di Lorenzo Nobile)

References

[1] Kahneman, D., Knetsch, J. L., & Thaler, R. H. (1990). Experimental tests of the endowment effect and the Coase theorem. Journal of Political Economy, 98(6), 1325-1348.

[2] Ericson, K. M. M., & Fuster, A. (2014). The endowment effect. Annual Review of Economics, 6(1), 555-579.

[3] Kahneman, D., Knetsch, J. L., & Thaler, R. H. (1991). Anomalies: The endowment effect, loss aversion, and status quo bias. Journal of Economic Perspectives, 5(1), 193-206.

[4] Künnapas, T. M. (1955). Influence of frame size on apparent length of a line.Journal of Experimental Psychology,50, 168–170.

[5] Tversky, A., & Kahneman, D. (1981). The framing of decisions and the psychology of choice. Science, 211(4481), 453–458.

[6] Kahneman, Daniel; Tversky, Amos (1979). “Prospect Theory: An Analysis of Decision under Risk”. Econometrica. 47 (2): 263–291

[7] Thaler, R. H., Tversky, A., Kahneman, D., & Schwartz, A. (1997). The effect of myopia and loss aversion on risk taking: An experimental test. The Quarterly Journal of Economics, 112(2), 647-661.

Rivista scientifica digitale mensile (e-magazine) pubblicata in Legnano dal 2013 – Direttore: Claudio Melillo – Direttore Responsabile: Serena Giglio – Coordinatore: Pierpaolo Grignani – Responsabile di Redazione: Marco Schiariti

a cura del Centro Studi di Economia e Diritto – Ce.S.E.D. Via Padova, 5 – 20025 Legnano (MI) – C.F. 92044830153 – ISSN 2282-3964 Testata registrata presso il Tribunale di Milano al n. 92 del 26 marzo 2013

Contattaci: redazione@economiaediritto.it

Le foto presenti sul sito sono state prese in parte dal web, e quindi valutate di pubblico dominio. Se i soggetti o gli autori fossero contrari alla pubblicazione, non avranno che da segnalarlo. In tal caso provvederemo prontamente alla rimozione.

Seguici anche su Telegram, LinkedIn e Facebook!

{kind=link}